In the intricate tapestry of mortgage lending, one metric has risen in prominence, especially in the realm of investment properties: the Debt Service Coverage Ratio (DSCR). For many loan officers, understanding DSCR can be the differentiator between approving an investment property loan or not. With AHL Funding’s dynamic offerings, like the AHL DSCO program, having a grasp on DSCR becomes even more pivotal. Let’s dive in and unravel the intricacies of the DSCR Ratio.

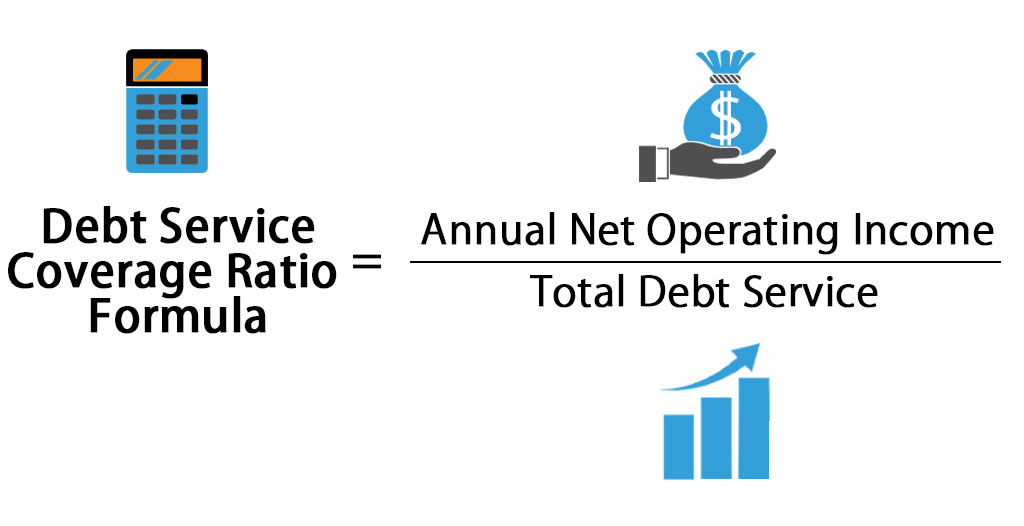

DSCR stands for Debt Service Coverage Ratio, a measure used primarily in the realms of commercial, multi-family, and rental property loans. It calculates the cash flow available to pay current debt obligations.

Formula: DSCR = Net Operating Income / Total Debt Service

AHL Funding, through its AHL DSCO program, utilizes the DSCR in a flexible manner:

Understanding DSCR isn’t just about mastering a formula; it’s about recognizing its significance in the broader context of property investment loans. With tools like AHL’s DSCO program, loan officers can confidently navigate the waters of investment property lending, ensuring both their clients and their institution are poised for success.

If you’re looking to elevate your knowledge and offerings in the lending landscape, consider AHL Funding’s array of programs tailored for modern financial scenarios. Begin your journey with AHL Funding’s Broker Approval. For those with specific queries or loan scenarios, seek prompt insights on the Submit a Scenario page, with AHL’s commitment to a 24-hour response, ensuring you’re always steps ahead in your lending journey.